A look at what is shaping our market views

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- The US economy still showing signs of ‘strength’

- The ‘speed’ of the economy going forward is in question

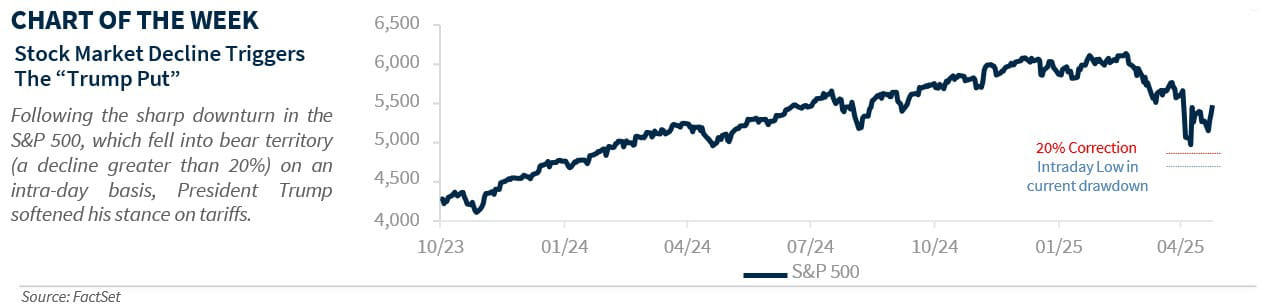

- Trump’s team shows some ‘flexibility’ on tariffs

Welcome to the Draft! The excitement is palpable as we head into the weekend, with teams revealing their top football picks and fortifying their rosters with fresh talent for the upcoming season. While 'draft night' steals the spotlight, the real action has been brewing for months with player assessments, interviews, and strategic planning in full swing. Think of the drafting process like investing—scouts meticulously rank players based on their strength, speed, flexibility, and mental acuity, much like we analyze the economy and financial markets to shape our outlook. The true value of these players might take years to unfold, just as investment results are best judged over the long term. But in the short term, despite the uncertainties and volatility brought by tariff concerns, here are some of the key ‘traits’ shaping our current market views.

- The US Economy Still Showing Signs Of ‘Strength’ | Despite a challenging first quarter, marked by a cold winter and a severe flu season, economic indicators suggest that the economy remains robust. Our 'Fab 5' indicators—withholding taxes, jobless claims, motor vehicle sales, and other real-time activity metrics—show a healthy labor market, continued consumer spending on big-ticket items like cars, and stable manufacturing activity. Interestingly, despite souring consumer sentiment, real-time activity indicators haven't shown any significant declines. Air traffic, restaurant bookings, and hotel occupancy are holding steady or even surpassing levels from last year. For the most part, this strength aligns with the results and management commentary from the 1Q25 earnings season so far. While uncertainty is affecting the outlook, banks and credit card companies report that consumers are still spending and corporate fundamentals remain solid. Because of this ongoing ‘strength’ in the economy, our base case remains that the US economy narrowly averts a recession (2025 US GDP Forecast: ~1%). However, if a recession materializes, our expectation is that it will be mild and short-lived.

- The ‘Speed’ Of The Economy Is In Question | Tariffs are the biggest wildcard for the economy. Because it's only been 3 weeks since most tariffs were announced, their impact has been limited so far. But this is likely to change soon. With container ships taking about 3-4 weeks to cross the Pacific Ocean, decreased supply from China and other global trading partners will soon be felt. For example, incoming cargo ships from China are on track to fall by about 35% YoY this month. The effects of reduced supply heading to ports may start showing up on store shelves by early summer. Additionally, some recent economic strength is due to a pull-forward in demand ahead of the tariffs (e.g., buying a car now to avoid tariffs), but this pace of spending is unlikely to continue. This suggests that growth headwinds are likely in the near future.

- Trump’s Team Shows Some ‘Flexibility’ | The Trump administration has become more ‘flexible’ with its trade rhetoric, especially after the April 2 reciprocal tariff announcements led to a major decline in the equity market (S&P 500 down ~20%) and a spike in interest rates (10-year Treasury yield up to ~4.60%). Despite saying they do not focus on the markets, these rapid movements likely revealed the pain threshold (i.e., the Trump put), prompting the administration to soften its aggressive policies. President Trump has since paused the higher reciprocal tariffs for 90 days, introduced technology exemptions, and suggested that the China tariffs (which soared to 145%) would be significantly reduced. The S&P 500's near bear market status negatively impacts net worth and hampers consumer spending and confidence. The sharp rise in interest rates raised concerns about the US losing its safe-haven status, and the president is aware that the US Government needs to refinance ~$8 trillion in debt, plus an additional $2 trillion after the debt ceiling is lifted by year end. So, higher rates would have made that more expensive. The administration's flexibility likely reduces the worst-case scenarios for the economy and financial markets.

- Consumer And Businesses ‘Mental Acuity’ Is Wavering | While optimism was high at the start of the year, the trade war has shaken confidence and impacted President Trump’s approval ratings. Ironically, his strength was once seen as his handling of the economy, but tariff uncertainty has pushed the approval rating on that issue to solidly below 50%. Tariff-related inflation anxiety has driven consumer confidence to a 4-year low. Policy uncertainty is also weighing on business confidence, as highlighted in this week’s Fed Beige Book report. The uncertain macro backdrop and rising input costs from tariffs have darkened the economic outlook. The longer these trade war concerns last, the greater the risk it could paralyze investment, hiring, and spending decisions, posing significant headwinds to growth. While sentiment may not be the best predictor of the economy, it has a significant influence on elections. If President Trump wants the Republicans to retain control of Congress, sentiment will need to improve considerably before next year's midterm elections.

Bottom Line | Despite worsening sentiment, the economy appears resilient and continues to grow, albeit at a slower pace, with the labor market remaining healthy. Therefore, we still believe the economy will narrowly avoid a recession in 2025, though it's a close call. However, the longer tariffs remain in place and uncertainty stays high, the risk of a more pronounced slowdown becoming a self-fulfilling prophecy increases—especially as tariff-related impacts start affecting consumers and businesses.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.